Are you aware that your credit score essentially dictates your financial destiny, influencing everything from your ability to secure a loan to the interest rates you'll pay? Your credit score is the cornerstone of your financial well-being.

The financial landscape is complex, a labyrinth of numbers and regulations that can often feel overwhelming. Among the most critical of these factors is your credit score, a three-digit number that significantly impacts your financial opportunities. This numerical representation of your creditworthiness acts as a key that unlocks doors to loans, credit cards, and even influences insurance premiums. Understanding and managing this score is not merely beneficial; it's essential for navigating the modern financial world successfully.

Consider this your introduction to a pivotal aspect of personal finance, a guide to demystifying the credit score and its implications. The goal is to equip you with knowledge, enabling you to make informed decisions and take control of your financial future.

- Hdhub4u Streaming Guide Is It Safe Legal Alternatives

- Top Ullu Web Series Actresses 2024 Names Photos Roles

The Anatomy of a Credit Score: Unveiling the Numbers

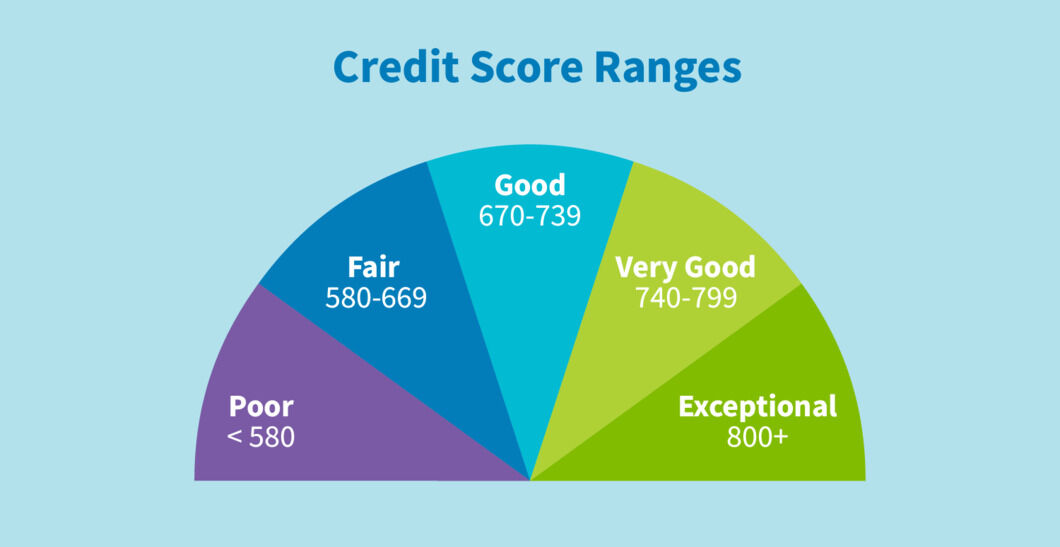

A credit score is not just a number; it's a comprehensive evaluation of your financial behavior, summarized into a single, easily digestible metric. It's a tool that lenders and creditors use to assess the risk associated with lending you money or extending credit. The most common credit scoring model is the FICO score, though other models exist, and they all share a similar range: typically, between 300 and 850 or 900. However, the specifics of how these scores are calculated, and interpreted, warrant careful consideration.

Understanding the tiers within this range is crucial. A score of 300 represents the lowest end, often indicating a history of severe financial mismanagement. As the score rises, so does your creditworthiness. Scores between 501 and 700 are often considered "fair," while those between 701 and 750 are generally categorized as "good." Scores above 750 are considered "very good" or "excellent," granting you access to the most favorable terms and interest rates. The higher your credit score, the better your chances of securing loans and credit cards, and the more advantageous the terms that you will receive. Conversely, a lower score can result in denial of credit or, if approved, higher interest rates and less favorable terms.

- Unraveling Fikfok Tiktok Confusion A Deep Dive

- Unveiling Top Ullu Web Series Your Guide To Mustwatch Titles

Building Blocks of Your Score: The Factors at Play

The mechanics behind credit scores is complex, but its foundation is built on five main factors, each carrying varying weight in the calculation. Understanding these factors can help you focus on the aspects of your credit behavior that need attention.

The first, and often most significant, factor is your payment history. This element tracks your history of paying bills on time. Consistent, on-time payments reflect responsible financial behavior and are viewed favorably by lenders. Late payments or defaults, conversely, can significantly and negatively impact your score.

The amount you owe, the second factor, looks at the amount of credit you are currently using relative to your total available credit. This is often expressed as your credit utilization ratio. A low credit utilization ratio, meaning you use a small percentage of your available credit, is generally viewed positively. Keeping your credit utilization below 30% is a good target, and ideally, you'd aim for below 10%.

The length of your credit history, the third factor, provides lenders with a longer-term perspective on your financial habits. A longer credit history generally indicates a more established track record. This component takes into account the age of your oldest credit account, the average age of all your accounts, and how long specific accounts have been open.

New credit, the fourth factor, is related to the number of credit applications you have recently made and the number of new credit accounts opened. Opening multiple new credit accounts in a short period can be seen as a sign of financial strain and can lower your score.

The final factor is the types of credit you use. A mix of different types of credit such as installment loans (like car loans) and revolving credit (like credit cards) may indicate responsible credit management, though this is a less influential factor compared to the others.

The Real-World Implications: How Credit Scores Affect Your Life

The impact of your credit score extends far beyond the realm of loans and credit cards. It permeates nearly every facet of your financial life, and the consequences of a low score can be substantial.

One of the most immediate effects is on your ability to secure financing. Whether you're looking to buy a car, a home, or even starting a business, your credit score is a primary consideration. Lenders use it to determine whether to approve your loan application and the terms, including the interest rate, you'll receive. A higher score means a lower interest rate, saving you potentially thousands of dollars over the life of the loan. Conversely, a low score can lead to denial or significantly higher rates, increasing the total cost of borrowing.

Lets take auto loans as a prime example. Applying online for a new or used car loan from capital one auto finance, for instance, is a common path for many. Lenders will scrutinize your credit score, credit history, and consider factors like the car's age. The rates you pay for auto financing are directly influenced by your credit score, with higher scores typically yielding lower rates. For instance, while this can fluctuate, someone with a 730 credit score might secure an average car loan interest rate of 6.70% for new cars and 9.63% for used cars, according to available data, a person with a credit score of 550 may face rates that are far less favorable.

Furthermore, credit scores can influence insurance premiums. Many insurance companies use credit-based insurance scores, which are derived from your credit report, to assess risk. A low credit score may result in higher insurance premiums for car insurance and home insurance.

Your credit score can also impact your ability to rent an apartment or secure employment. Some landlords and employers use credit checks as part of their screening processes, making a good score essential. A low score could lead to a denial of housing or job opportunities.

How to Improve Your Credit Score: A Practical Guide

Improving your credit score isn't an overnight process; it requires a consistent and disciplined approach. But it's achievable, and the rewards are significant. Here are some actionable steps to take:

First, and foremost, pay your bills on time, every time. This is the single most important factor in building and maintaining a good credit score. Set up automatic payments, create reminders, or do whatever it takes to avoid late payments.

Manage your credit utilization. Aim to keep your credit card balances low, ideally below 30% of your credit limit. If possible, keep it even lower, such as 10% or less.

Review your credit report regularly. You are entitled to a free copy of your credit report from each of the three major credit bureaus Experian, Equifax, and TransUnion once a year. Check for errors and dispute any inaccuracies promptly. These errors can negatively affect your score, so it's crucial to correct them.

Avoid opening too many new credit accounts at once. This can signal financial risk to lenders. Space out your applications for new credit to avoid negatively impacting your score.

Become an authorized user on a credit card account with a good payment history. This can help you build credit, but ensure the primary cardholder manages the account responsibly, as their behavior affects your score.

Don't close old credit card accounts. The length of your credit history is a factor in your credit score, and closing older accounts can shorten your credit history and potentially lower your score.

Gomyfinance and Simplifying Bill Payments

Managing your finances, including paying bills on time, can be made easier through various tools. Gomyfinance offers easy tools to manage bills effectively. Overdraft charges can occur if you don't track your bank balance, and it's best not to be disorganized. Gomyfinance can streamline bill payments and can be useful in this regard, it can provide a way for you to centralize your bill payments, track due dates, and potentially automate these tasks.

Credit Score Variations and Monitoring

It's essential to understand that credit scores may vary between different credit bureaus. You can have an Experian score of 750 or above but may be below 700 in another agency's report. Therefore, keep a tab on credit scores from multiple bureaus, and check them regularly, preferably once every month. Similarly, different lenders may have their own benchmark of a 'good' credit score. Checking your credit score can help you gauge your loan approval chances. Understanding your credit history and current credit score may help you make a more informed decision on your auto loan.

Where to Find Help

Whether you're new to the concept of credit scores or looking to improve yours, resources are available to simplify the process. Gomyfinance.com credit score services, for example, provide definitions, importance, and tools for better credit management. Consider this a crucial step for beginners. Think of your credit score as a financial report card lenders use to decide whether to approve your loans or credit cards.

If you're looking to secure financial products, such as auto loans, remember that lenders will take into account your credit score, credit history, and other factors. You will ultimately be approved or denied. The essential guide for beginners will show you how to check spelling or type a new query. Don't forget that a credit score is a numerical representation of your creditworthiness.

Disclaimer: Please note that this article is intended for informational purposes only and does not constitute financial advice. Consult with a financial professional before making any financial decisions.

- Diva Flawless Xxx Video Truth Analysis What You Need To Know

- Ullu Web Series Your Ultimate Guide To Streaming More